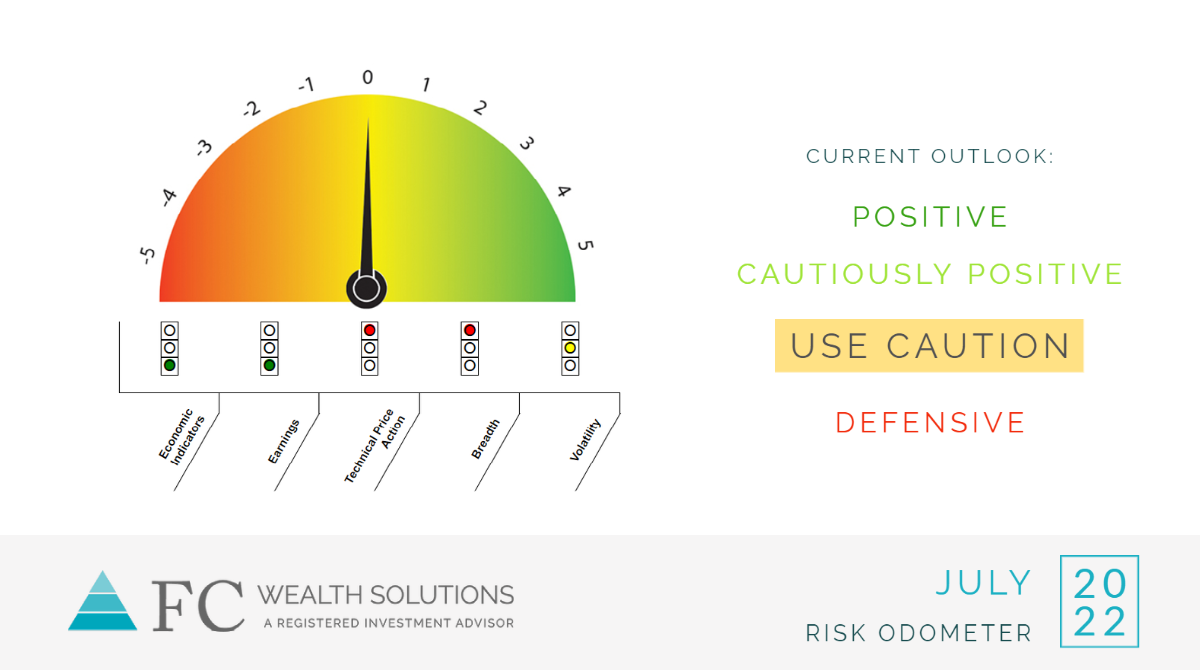

For the 3rd month in a row, our Risk Odometer is unchanged at 0 with a Current Outlook of “Use Caution”. We continue to witness conflicting signals which gives us caution. Our more sensitive and timely technical indicators are displaying caution. Our longer-term, fundamental indicators remain positive. Until this conflicting battle finds a winner, we will remain with a degree of caution and uncertainty in our outlook.

We have said in our previous Risk Odometer Blogs that we felt the stock market would look attractive if it entered official “bear market” territory, defined as a 20% drop of the S&P 500 from its all-time high. We prefaced that bullish call by adding “as long as the economy was not headed toward an imminent recession.” We officially entered a bear market last month…but recent economic reports are now showing a high likelihood of us also entering a recession (two consecutive quarters of economic contraction). So where does that leave us in our outlook going forward?

For long-term, strategic investors, which we define as having greater than five-year horizons without much concern for volatility over shorter time periods, we would argue that buying stocks during a recession has been a good idea from a historical perspective. For that type of investor, the markets are likely offering you good opportunities to invest today. Those drawdowns were all eventually fully recovered thus providing the investor a good entry point. Be careful though. Most investors say they are long-term and are not bothered by short-term volatility only to change their feelings and actions when they experience it. This is the biggest mistake amateur investors make.

For more tactical investors, those with horizons less than five years, and those who seek to manage downside risk, we remain cautious over the near-term. Our sensitive technical indicators such as Price Action, Volatility and Breadth remain well in cautious territory. Fundamental data, while still positive in our Risk Odometer, are starting to roll over. Economic growth is likely to contract for the second quarter of 2022, which would technically put us in a recession.

On the flip side of the contracting economy, the contraction looks very mild compared to most recessions. The labor market remains strong, and consumer’s balance sheets are still healthy given the large amount of stimulus injected into the economy during Covid, boosting savings rates, thus providing cushion to an economic slowdown. Also, the economy is actually still growing, it is just not growing as fast as inflation. Recessions are calculated based on “real” terms, whereby they subtract inflation from nominal growth. With inflation at 8%, tipping into a recession is quite easy, but it does not imply steep contractions in nominal growth. For these reasons, we do not believe tipping into a recession has to guarantee further significant stock market losses. In 1994 the economy experienced a mild recession and the stock market only contracted 20%, less than what we have already contracted.

In summary, we remain cautious over the near-term as negative technical indicators and deteriorating fundamental indicators provide enough uncertainty to make us cognizant of potential further downside. We do not envision that potential downside as draconian nor outside of something that market has experienced in the past and fully recovered, so we believe there is good value for the long-term investor at current levels. Our experience has taught us that many investors say they are long-term but react more like short-term investors. For this reason, we seek to manage downside risk during periods of uncertainty, an environment we find ourselves today.

As always, we continue to believe our Risk Odometer provides guidance in making better investment decisions because it keeps us objective and disciplined. We use this methodology and advise our clients to do the same. Emotions are our enemies in investing.

It is important to understand that our Risk Odometer is not designed to anticipate small to medium corrections, typically those in the 5-15% range. Instead, it monitors for conditions which have typically preceded larger corrections. We believe trying to anticipate small to medium corrections sounds attractive but more often results in lost opportunity than savings.

The Equity Market Risk Odometer is our guide for judging risk in the equity market. It is used as a guide for investment decisions in our proprietary investment strategies. It is composed of various indicators based on leading economic indicators, earnings, technical price action, breadth, and volatility. Its score can range from +5 to -5. Readings greater than 1 are positive and readings less than or equal to zero are negative.

Disclosures

This information does not have regard to the specific investment objectives, financial situation and the needs of any specific person who may view this information. Statements, opinions, and forecasts made represent a particular observation and assessment of the market environment at a specific point in time and are not intended to be a forecast of future events or a guarantee of future results. Statements regarding future prospects may not be realized and may differ materially from actual events or results. Past performance is not indicative of future performance.

FC Wealth Solutions and its representatives do not provide legal or tax advice. You may want to consult a legal or tax advisor regarding any legal or tax information as it relates to your personal circumstances.

Michael Fickell is an investment advisor representative of FC Wealth Solutions

Securities and investment advisory services offered through FC Wealth Solutions, a registered investment advisor.

CRD#: 4209688