2017 | April Risk Odometer

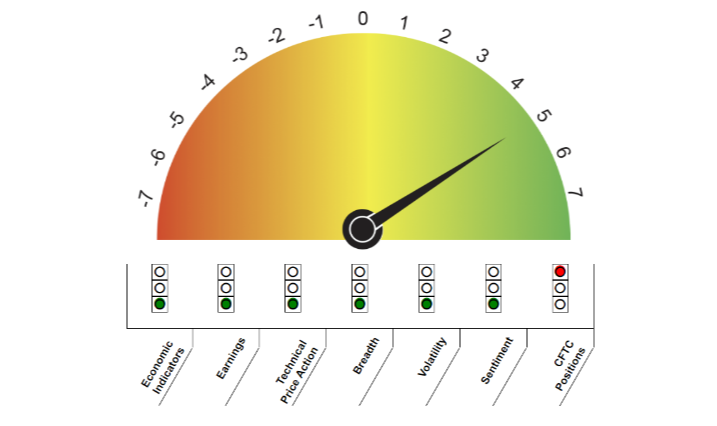

Equity Market Risk Odometer*

April 2017 Monthly Summary

- Equity Market Risk Odometer continues to display widespread positive conditions

- Markets rally post the French elections

- Popular Trump election trades continue to lose ground.

- Geopolitical tensions rise in North Korea and Syria

Equity Market Risk Odometer: The Equity Market Risk Odometer finished the month was a net reading of +6, well into positive territory and continuing to signal strong underlying conditions for equity markets. The odometer’s Four Core Indicators (Economic Indicators, Earnings, Technical Price Action and Breadth) all continue to remain positive, further confirming the strong net overall reading. Only one category (CFTC Positions) is flashing warnings, but this is easily cancelled out by the six other positive categories.

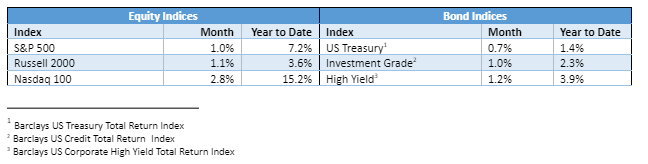

Markets: The month of April witnessed several geopolitical events that would normally keep equity market participants away from the buy button. They temporarily did but French elections late in the month removed a large amount of uncertainty, helping to propel both equity and bond markets higher in April. For the month, the S&P 500 finished 1% higher. The big winner following the French elections were overseas markets. Developed international markets rallied 2.5% in April and emerging markets rallied 2.2%. International equity markets, which had largely underperformed since the lows in 2009, continue to outperform domestic markets this year. The bond market also continues to perform well following its sell-off late last year. The aggregate bond benchmark was up 0.8% on the month and 1.6% on the year.

Popular Trump election trades continue to lose ground this year following their tremendous rally after November’s election results. Small Cap US Stocks, which rallied nearly 16% in the final two months of 2016, have lagged this year, up only 3.6%. International and emerging equity markets, which experienced losses following the US presidential election, have continued to outperform this year, up 10.0% and 13.9% year to date. Much of this reversal has been the realization that campaign promises and legislative results are very different. Trump swept into office with lofty expectations and was determined to fulfill those promises immediately. What he has experienced so far is a fractured Republican Party and Democrats steadily aligned to block every possible move. The end result has been a lack of significant legislation and an unwinding of popular post-election trades. (A detailed synopsis of his first 100 days in office can be found here.)

Economic Developments: The US and global economies continue to perform well, which has helped keep a floor under the markets for the year. First quarter US GDP registered a disappointing 0.7% annualized but this was largely discounted as temporary and backward looking. Forward looking indicators and business sentiment readings remain high, painting an optimistic outlook for the quarters ahead. In Europe and the UK, manufacturing sentiment rose to their highest level in six and three years respectfully, also painting an optimistic outlook for global markets.

Other Developments: One the geopolitical front, the President has taken a very different stance from his predecessor. He has ratcheted up the pressure on North Korea to end their nuclear weapons campaign and launched massive bomb raids on ISIS, dropping the “mother of all bombs” in Afghanistan.

He also ordered 50 tomahawk missiles to be fired into Syria in response to their governments use of chemical weapons. The Syrian strike has continued to create strained relations with Russia, who is actively involved in warfare inside of Syria. On the US political front, Trump announced a broad outline of his tax proposal, which looked more like the opening round of a negotiation rather than actual policy, and Congress struck a budget deal that largely neglected the President’s main priorities.